COVID-19: Attitudes, Behaviors, and Expectations Survey

Published in ATÖLYE Insights · 15 min read · May 31, 2020

Findings and insights found in the behavioral change research conducted by ATÖLYE between April 10 - 22.

Survey design, data analysis, and authorship of the findings: Selim Aykut, Director, ATÖLYE Dubai Translation: Gizem Ünsalan Editor: Ömer Ataş Data visualization: Selim Aykut, Funda Çevik Dinsdale

Scope of the Survey

This survey was held from April 10 to 22 via an online questionnaire accessed mostly via LinkedIn, Twitter, and Facebook. A total of 1740 respondents, most of them residing in Turkey, contributed to the study.

The topics featured in the survey focused on determining how COVID-19 altered our daily lives as well as the overall impact of this global pandemic on our attitudes, behaviors, and expectations from the future.

The respondents' age distribution closely reflected that of the overall population. That said, when we consider the platforms through which we reached out to respondents, as well as their employment status and level of financial savings, it would be useful to assess the findings and insights of our survey based on the subset of individuals "with high digital literacy and frequent social media use, who work (or have worked) in professional industries," rather than the population at large.

A brief summary...

- Although the coronavirus (SARS-COV-2) infects members of society indiscriminately, the economic, sociological, and psychological problems triggered by the COVID-19 pandemic have a vastly different impact on the different groups within society. Especially for young people, students, and freelancers who haven't been able to secure their future financially, the fight against COVID-19 is proving to be a much more challenging and destructive process.

- COVID-19 is not just a health problem. Nearly 50% of respondents report that, in the event of loss of income, their financial savings could "sustain" them for 3 months at the most. In addition to the government, individuals, companies, non-governmental organizations - in short, all stakeholders in society - will need to assume responsibility and (similar to the logic of flattening the curve) they must contribute to flattening the curve of the economic toll.

- "Remote work" is the most fundamental change in the lives of workers. However, this doesn't mean the same thing for everyone. Seeing as how this model will continue to be a part of work life post-COVID-19, it will need to be customized, formulated, and designed according to the different needs of individuals and institutions.

- "Payrolled employees" trust their employers to "do the right thing" during the COVID-19 period. As the economic burden caused by the pandemic grows heavier, the precautions taken by employers in order not to break this trust hold critical importance both in terms of employees' health as well as the future of institutions and society.

- Behaviors and habits are changing; "Cooking at home" and "being prudent with money" are the two behaviors most widely adopted by respondents during this time. However, the psychological impact of this period is also starting to emerge. 40% of respondents report disrupted sleep schedules, increased food consumption, and difficulty concentrating.

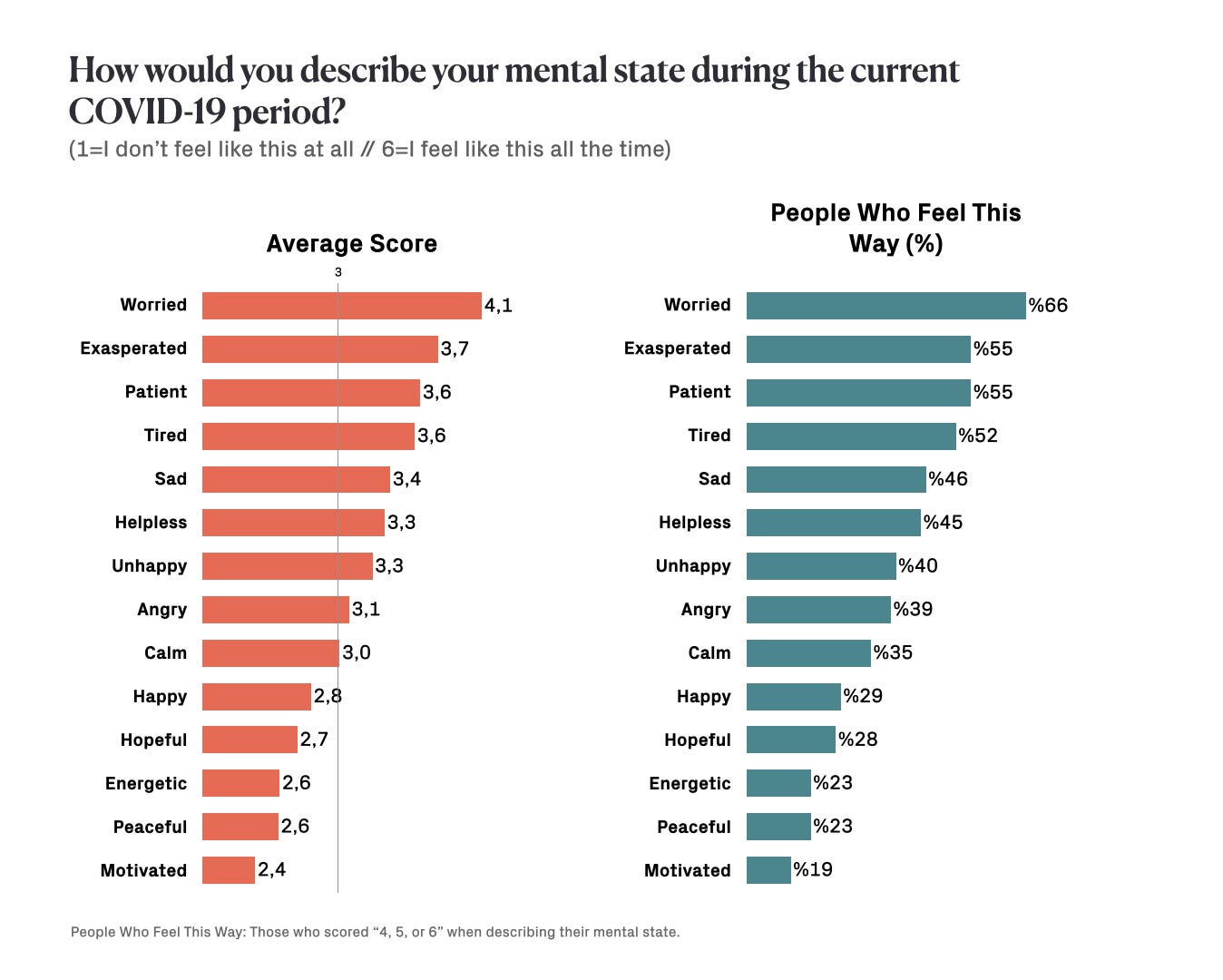

- 66% of respondents are "worried," 55% are "exasperated," and 52% are "tired." At 55%, the only "positive" mental state to emerge is "patience." Those who have engaged in activities to maintain their physical and mental health during this time have a much better overall mental state compared to those who have not engaged in any activities. "Maintaining our mental health" will have to be a key area of focus for us in the upcoming term.

- 42% of respondents expect to "return to normal" latest by the end of June, while 78% anticipate it will happen latest by the end of September. In the event that the pandemic is prolonged and a return to "normal" isn't possible some time, the impending gap between expectation and reality poses a societal risk. Another major area of focus is guiding public expectation in a healthy way, using the most accurate information at hand.

We might be facing the same storm, but we are not all in the same boat.

Financial Outlook

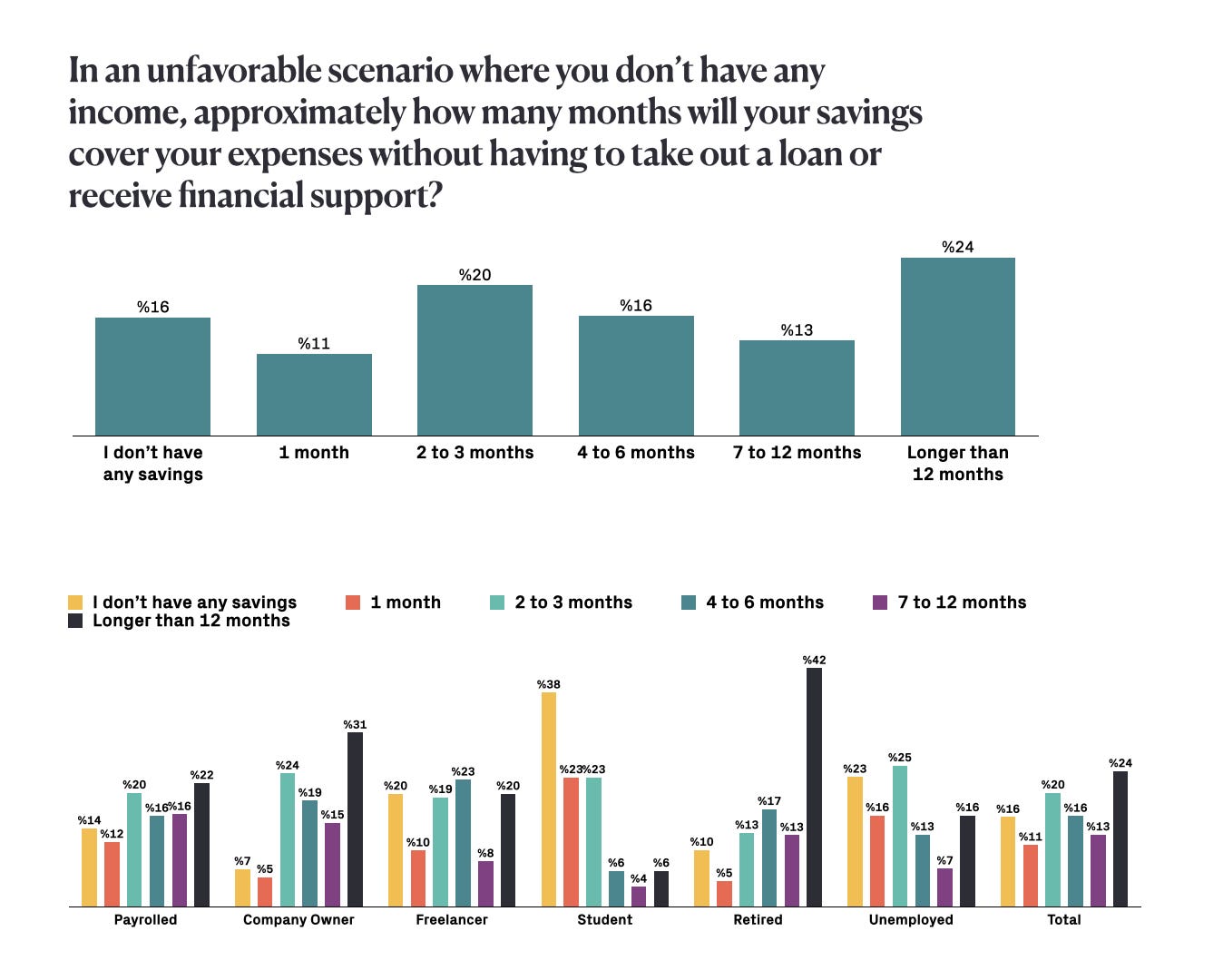

In the event of loss of income, 47% of respondents report having financial savings that could "sustain" them for 3 months or less.

Only 24% of respondents can survive for 12 months or longer in the event of loss of income.

20 to 38% of freelancers, students, and unemployed individuals report that they have no savings.

These three subgroups are the ones that will need the most support during the economic crisis already under way.

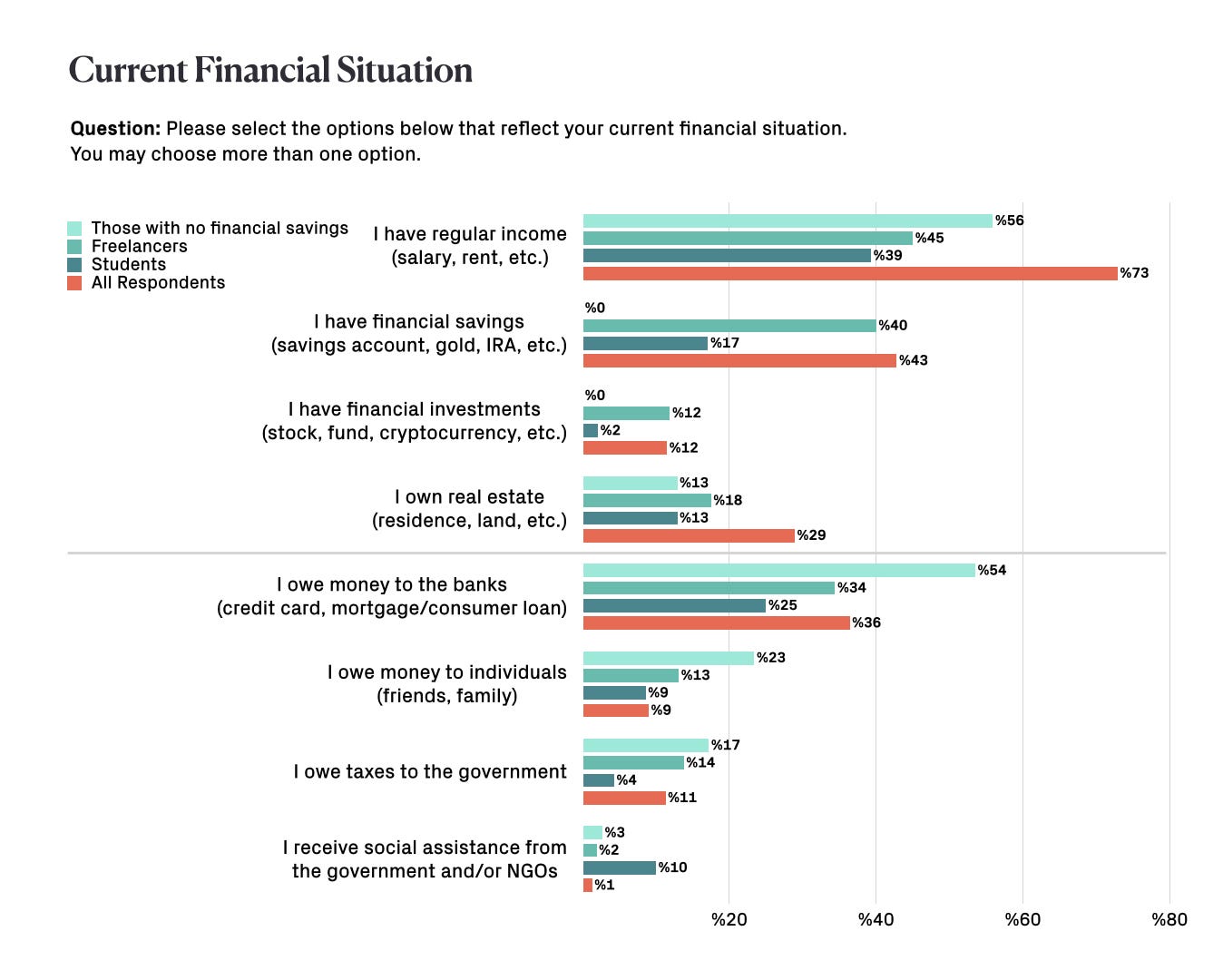

73% of respondents report having regular income, while 36% are indebted to banks, 9% to individuals, and 11% to the government.

43% of respondents have financial savings, 12% have investments, and 29% own real estate.

Only 56% of those without any savings have regular income, while 54% are indebted to banks. For this group of people, any incoming money goes straight to sustaining daily life.

45% of freelancers have regular income, while 40% have financial savings. Similar to the overall average, one out of three freelancers is indebted to banks.

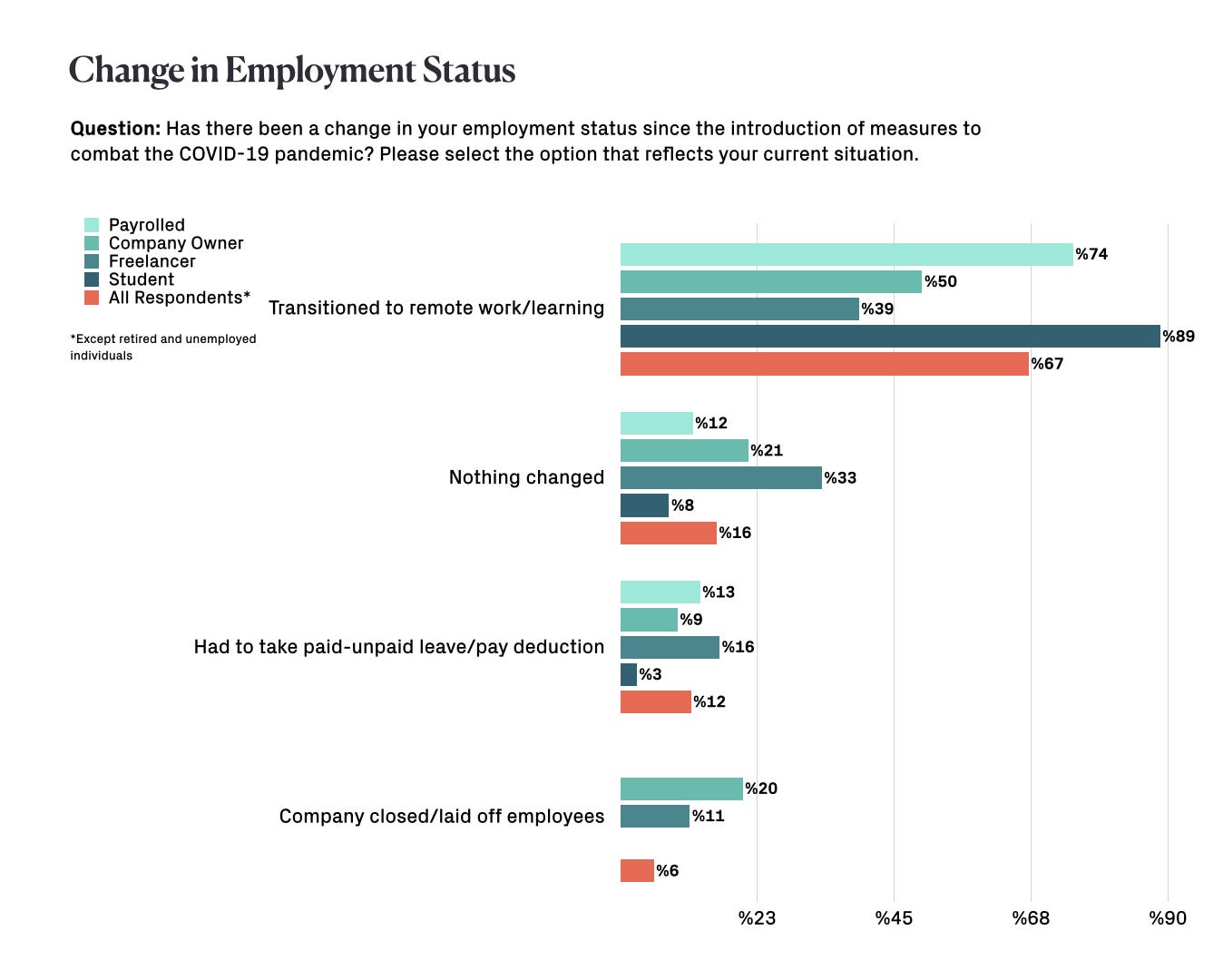

Change in Employment Status

In conjunction with measures to prevent the spread of COVID-19, 74% of payrolled employees and 89% of students have transitioned to remote work and learning.

Fewer company owners (small businesses) have transitioned to remote work compared to payrolled employees. Meanwhile, freelancers - who worked remotely prior to COVID-19, as well - are the group whose circumstances changed the least.

Between the dates of April 10 and 22, when the survey took place, 12% of respondents had to take compulsory leave or undergo a deduction of pay/rights (the rate is 16% among freelancers).

As of the beginning of May, when this report was put together, it is - unfortunately - highly likely that these rates might have gone up.

20% of company owners report that they had to either shut down their business or lay off employees in April. As the economic impact of the pandemic becomes more pronounced, it unfortunately seems inevitable that these rates will go up.

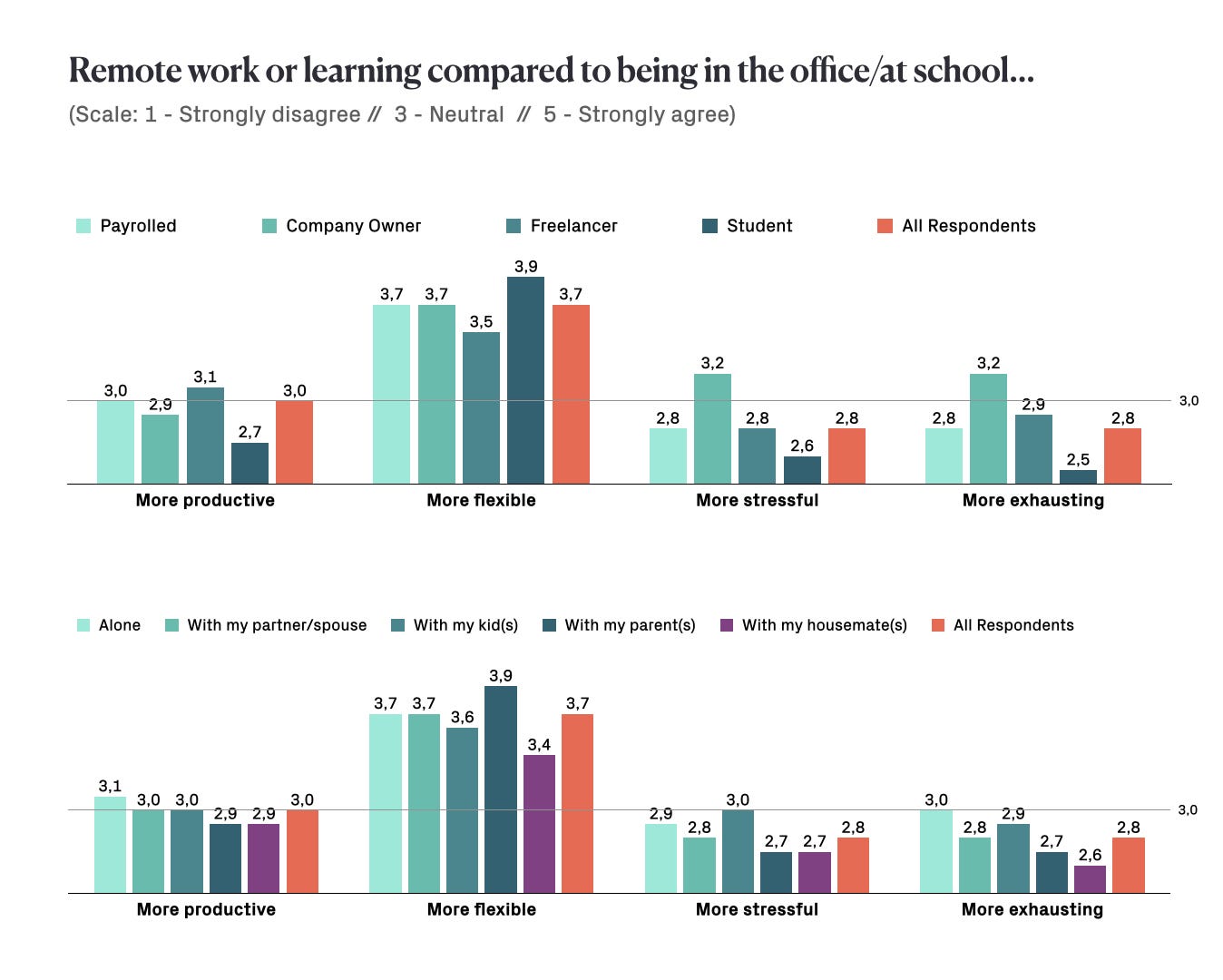

Remote Work and Trust in Employers

All groups who transitioned to remote work/learning unanimously agree that this model is "more flexible."

When it comes to productivity, the opinion is currently "ambivalent." However, students, in comparison to other groups, believe that remote learning is not productive.

Compared to all other groups, company owners find remote work to be both more stressful and more exhausting. Many companies unaccustomed to remote work are struggling, as they had to shift to this model suddenly and without preparation.

Respondents who live with their kids find remote ork to be more stressful compared to other groups.

Meanwhile, those who live alone report that this model is relatively more productive yet more exhausting. "Working from home" likely turns into "working constantly from home," blurring the boundaries of regular work hours.

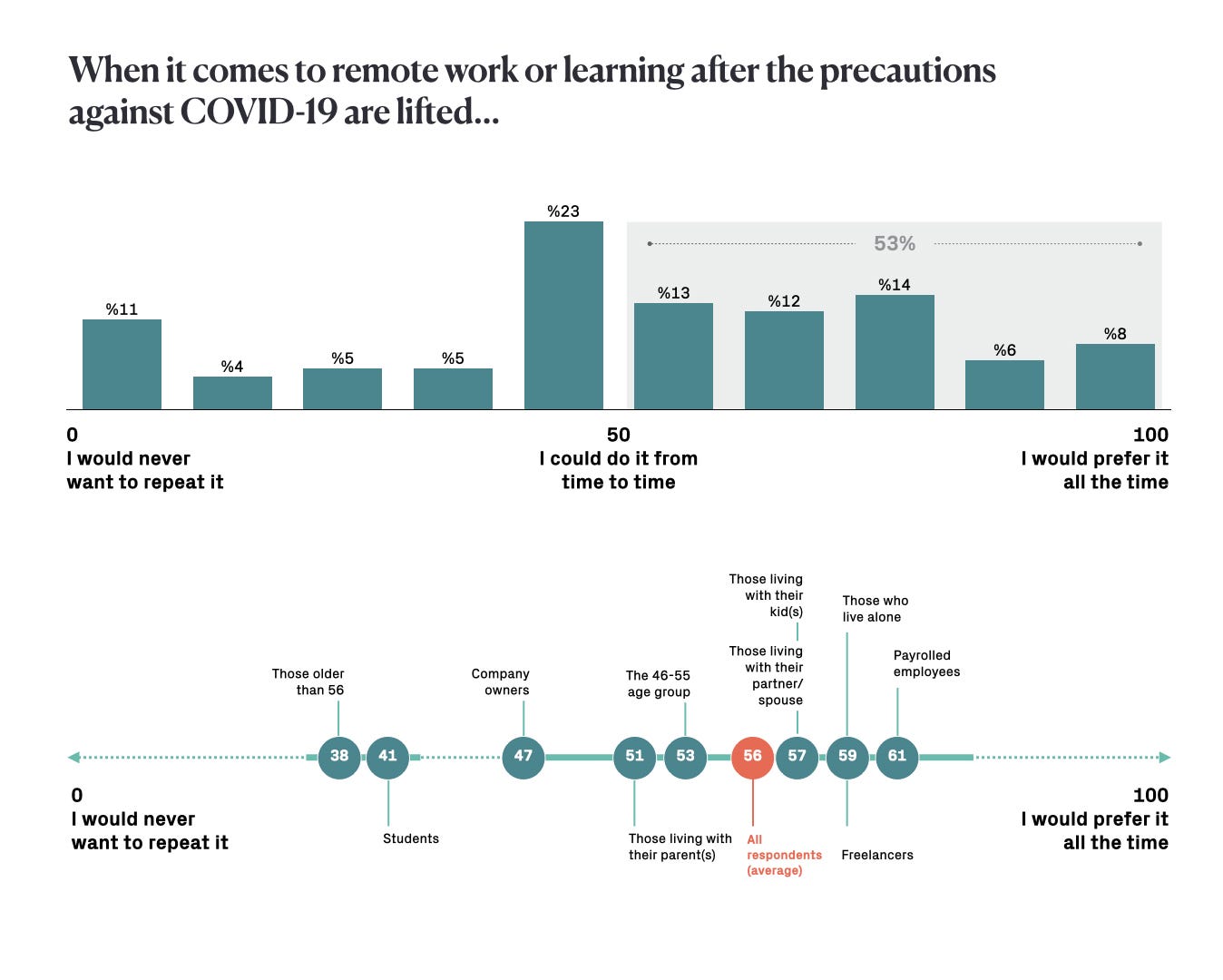

53% of respondents report that they would prefer to work/learn remotely even after COVID-19. Meanwhile, 14% would prefer switching to this model almost entirely.

When we look at the average for all respondents, we could conclude that there's a willingness to work from home 2 to 3 days out of every 5 business days (56 out of 100).

Those who would prefer to work remotely in the future are payrolled employees, freelancers, and those who live alone.

Meanwhile, those who do not prefer this model are respondents older than 56, students, and company owners.

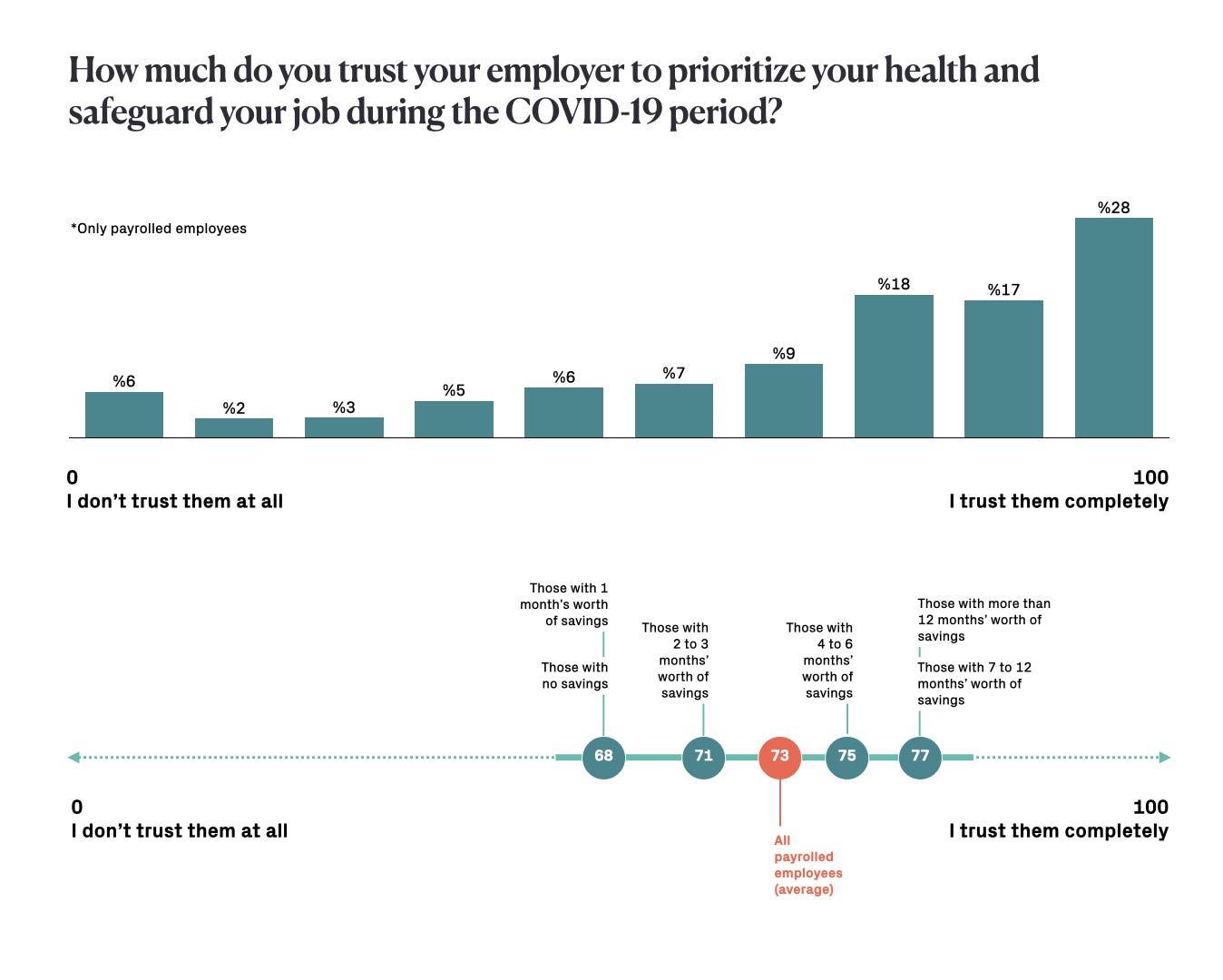

Payrolled employees have a high rate of trust in their employers, with an average score of 73 out of 100.

When we consider that the majority of respondents are from professional industries, it would be useful to assess this trust on the basis of "white collar" workers.

Looking at the breakdown of "Financial savings to cover expenses in the event of loss of income," we see a positive correlation between financial savings and trust in the employer.

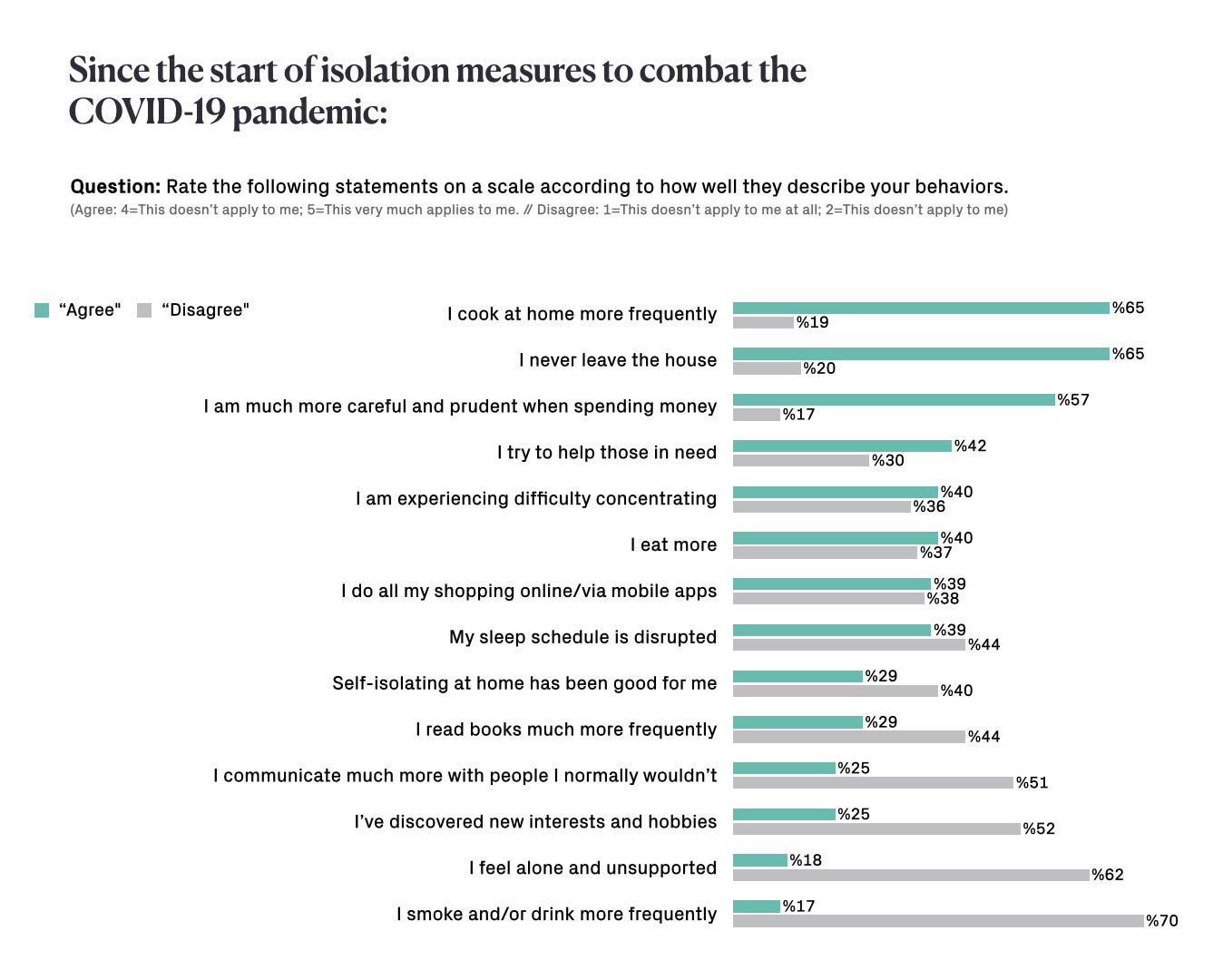

Behaviors and Habits

The most fundamental habit that changed along with pandemic precautions is "cooking at home," with 65% of respondents preparing meals at home more frequently.

Another significant change is spending: 57% of respondents are much more careful and prudent in their expenditures. We will soon see the effects of this, particularly on the retail industry.

39 to 40% of respondents report disrupted sleep schedules, increased food consumption, and difficulty concentrating. Moreover, 18% of respondents feel alone and unsupported - here, we're also beginning to see the impact of psychological distress on behavior.

On the other hand, 25 to 30% of respondents report that they're reading more books, discovering new interests and hobbies, and overall benefiting from self-isolation at home. In short, isolation doesn't affect everyone the same way.

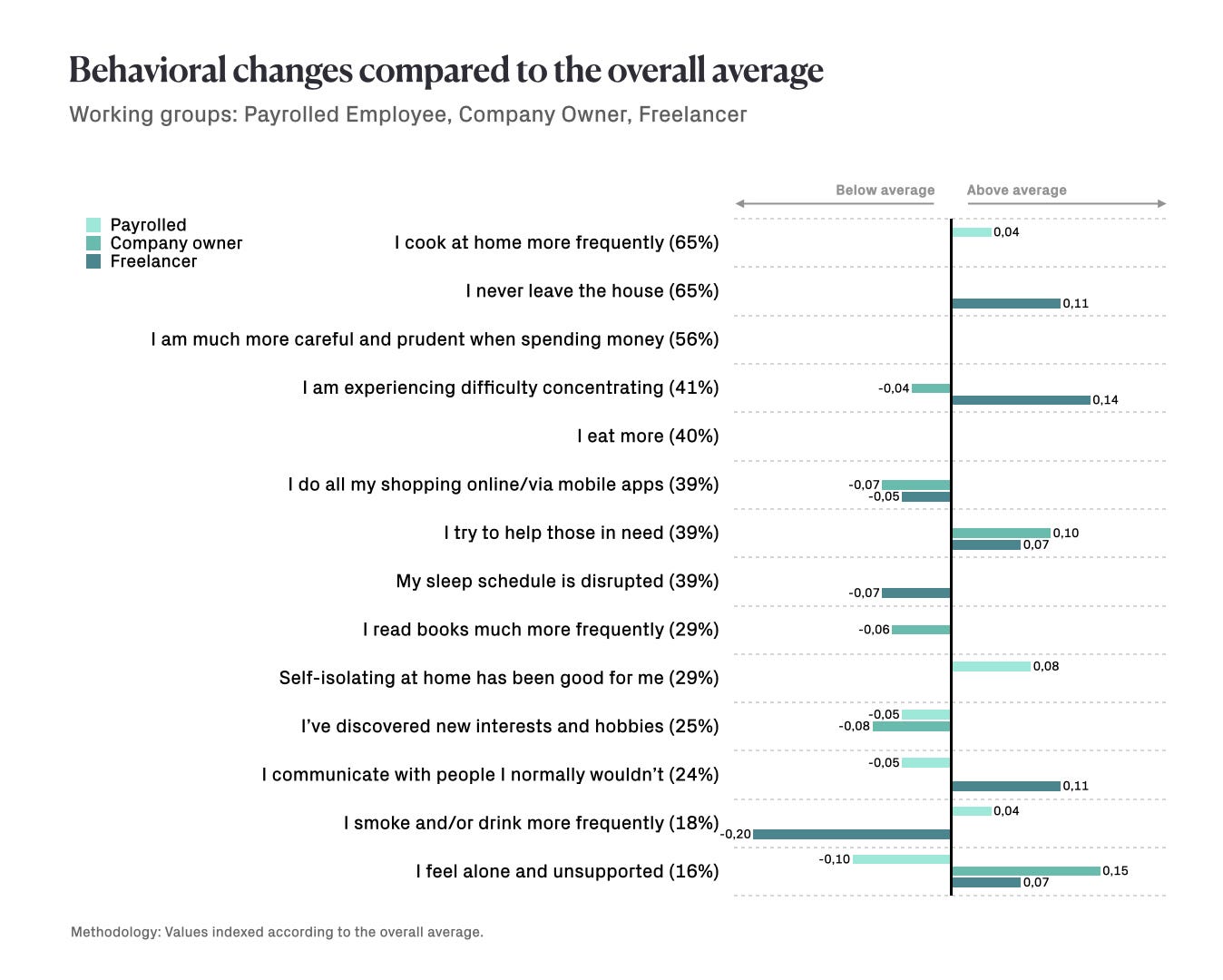

Some insights pertaining to the groups who work, compared to the overall average of all respondents:

- Freelancers are having difficulty concentrating, talking to people they normally wouldn't (perhaps to take on "new projects"), and feeling relatively alone and unsupported.

- Self-isolating at home has been better for payrolled employees.

- Company owners feel alone and unsupported, yet they're also trying to help those in need.

Some insights pertaining to the groups who don't work, compared to the overall average of all respondents:

- Students are more careful and prudent when spending money. They shop online. Students are also the group who feels most alone and unsupported.

- Retirees have less difficulty concentrating compared to other groups; they've discovered new interests and hobbies, and they communicate with people they normally wouldn't. Retirees are also the group who feels the least alone and unsupported.

- The unemployed are having difficulty concentrating as well as drinking and/or smoking more. They also feel alone and unsupported, although not to the extent that students do.

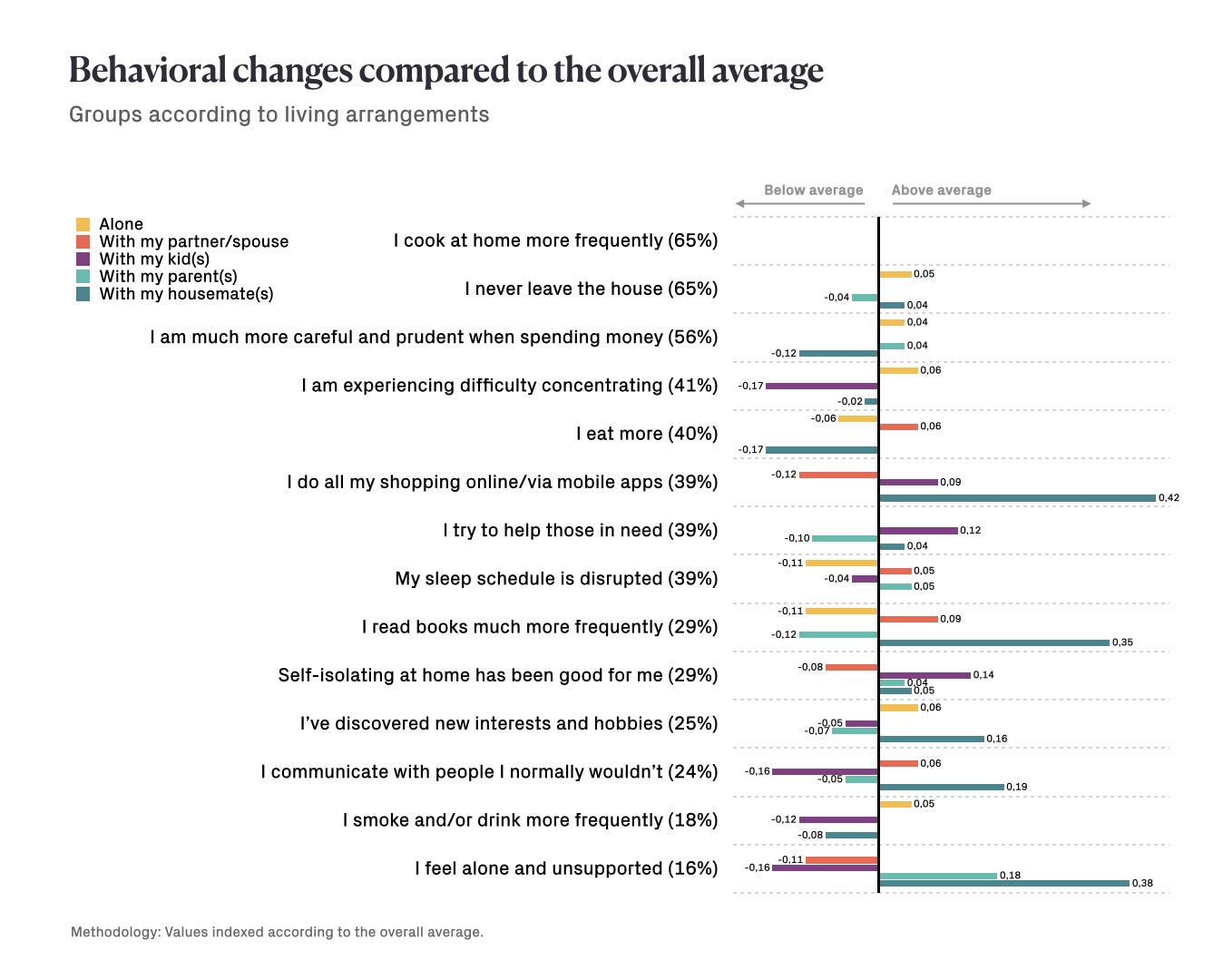

Some insights pertaining to living arrangements, compared to the overall average of all respondents:

- Those who live with their kid(s) are benefiting more from self-isolating at home; they don't have as much difficulty concentrating, and they feel less alone and unsupported.

- Those who live with housemates (mostly students) are less prudent in spending, yet they feel more alone and unsupported. They are also the group doing the most online shopping.

- Those who live alone have less disrupted sleep schedules, leave the house less frequently, and have discovered new interests and hobbies the most.

When we look at financial savings compared to the overall average of all respondents, we see that the groups with little savings are those who experience the most psychological distress (disrupted sleep schedules, difficulty concentrating, feeling alone and unsupported, alcohol and/or tobacco consumption).

Due to reasons pertaining to income level, this group also has trouble "staying home," cannot spend money prudently, and is unable to support others.

In this regard, it helps to view the pandemic not just as a health crisis but as a triggering factor for a larger psychological and socio-economic crisis - and to concentrate our efforts around generating solutions in a more holistic framework.

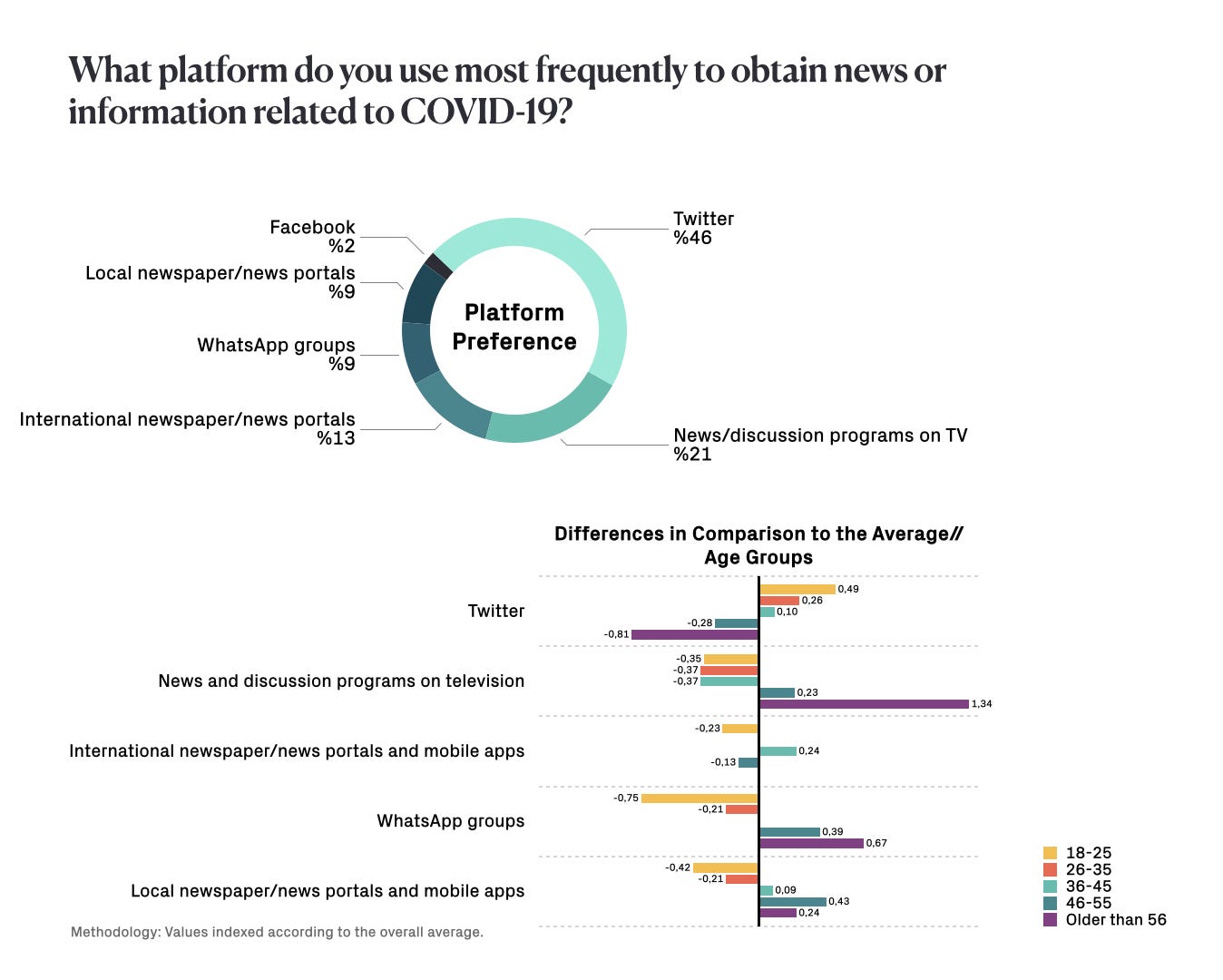

Since we reached out to respondents via social media platforms, it's only natural that 46% of respondents use Twitter the most.

When we look at platform use by age group compared to the overall average, we see that, as age increases, the use of Twitter as the primary source of news decreases, with television, WhatsApp groups, and local newspapers becoming more prominent.

These findings coincide with general trends regarding the use of these platforms.

Mental State

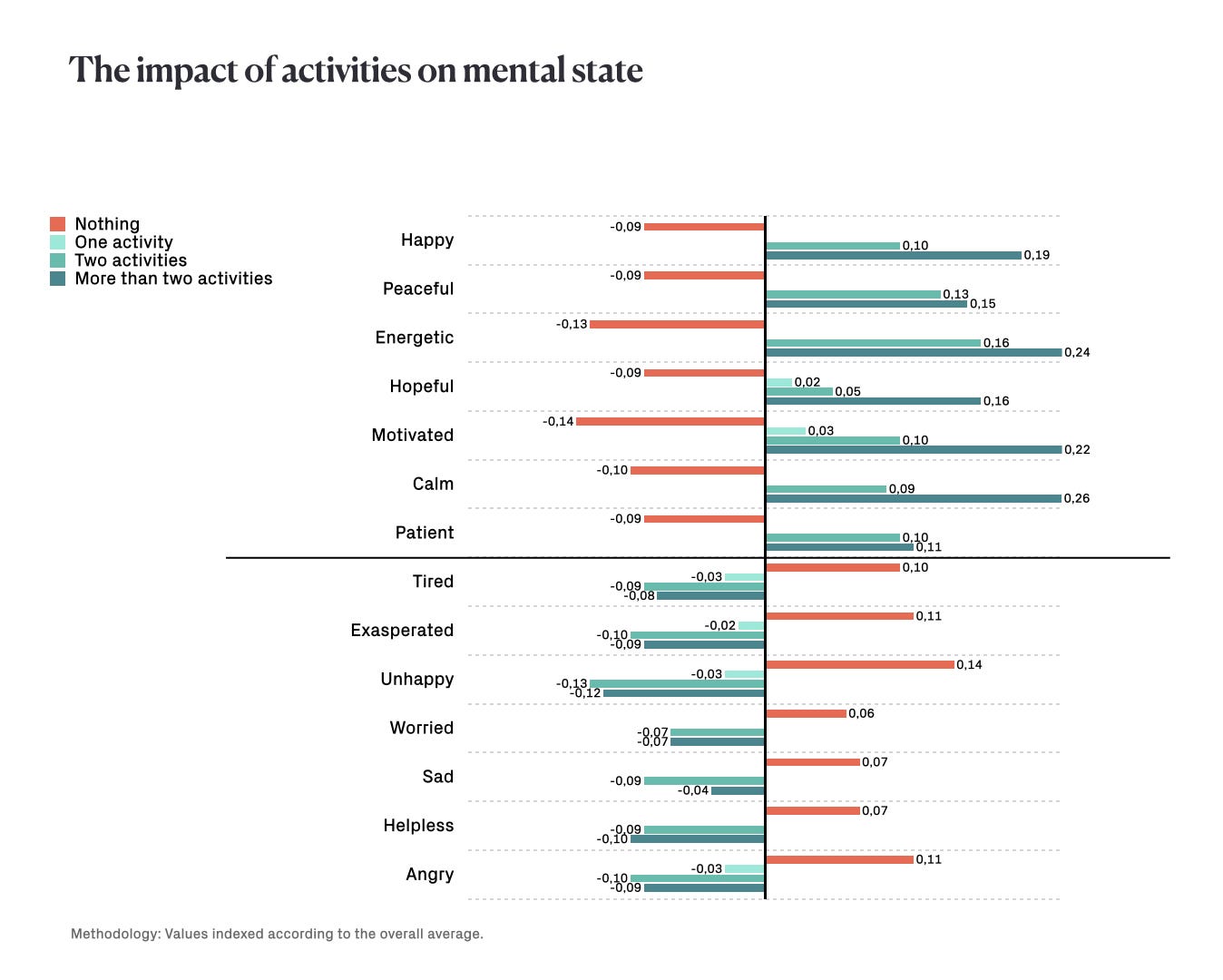

On the whole, respondents' mental state is substantially negative: 66% are worried, 55% are exasperated, and 52% are tired.

At 55%, the only "positive" mental state that emerged is patience.

Around 20% of respondents reported feeling motivated, peaceful, and energetic.

By contrast, 45–46% are helpless and unhappy, while 40% are angry.

If prolonged (as feared), the COVID-19 period bears the risk of significantly and negatively impacting people's mental state.

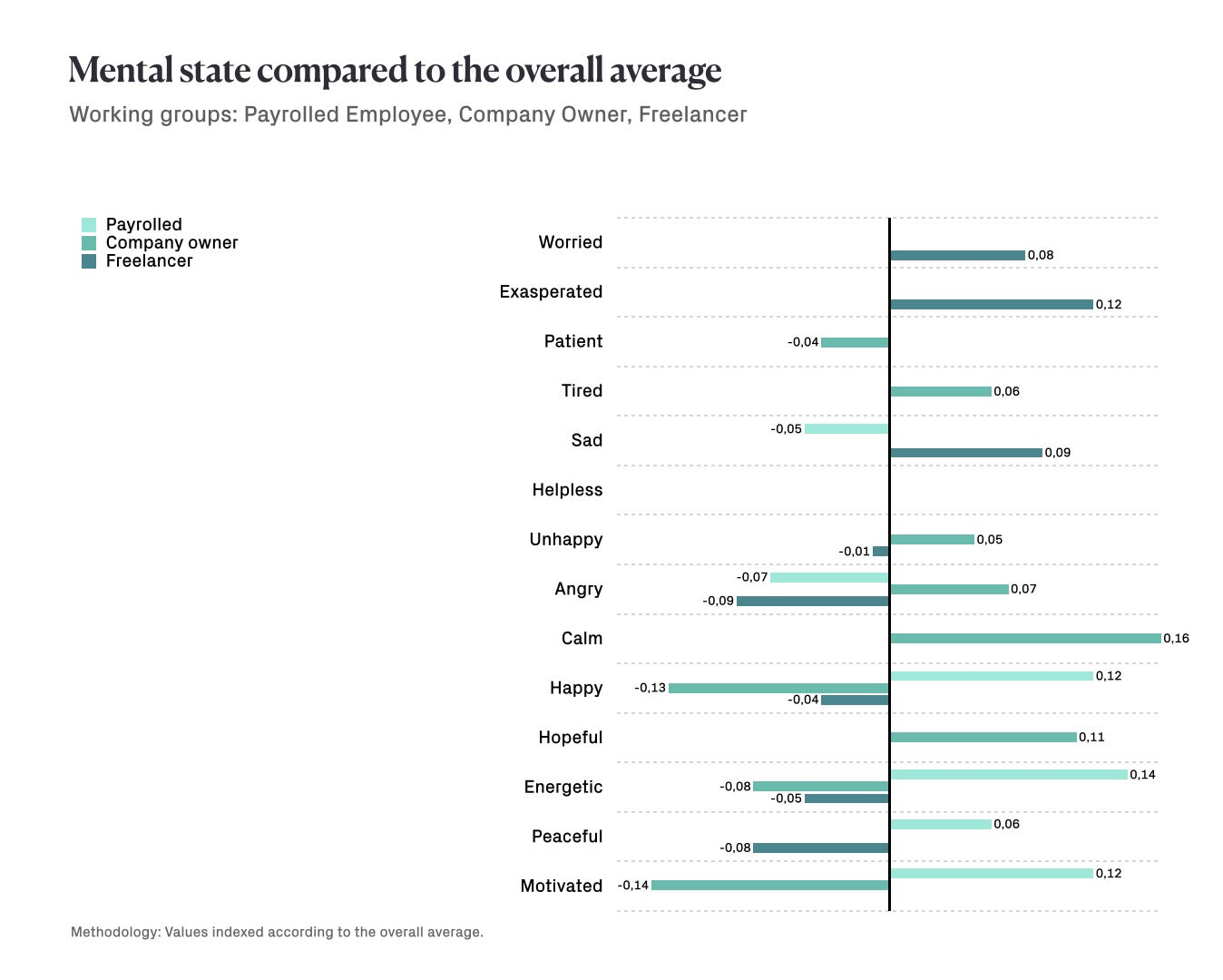

Some insights pertaining to working groups, compared to the overall average of all respondents:

- Freelancers are more worried, more exasperated, and overall sadder.

- Company owners are unhappier, angrier, and experiencing a serious lack of motivation. However, due to experience brought by age and past crises, they are calmer and more hopeful compared to the overall average.

- Payrolled employees are a little happier, more hopeful, energetic, and motivated when compared to the overall average.

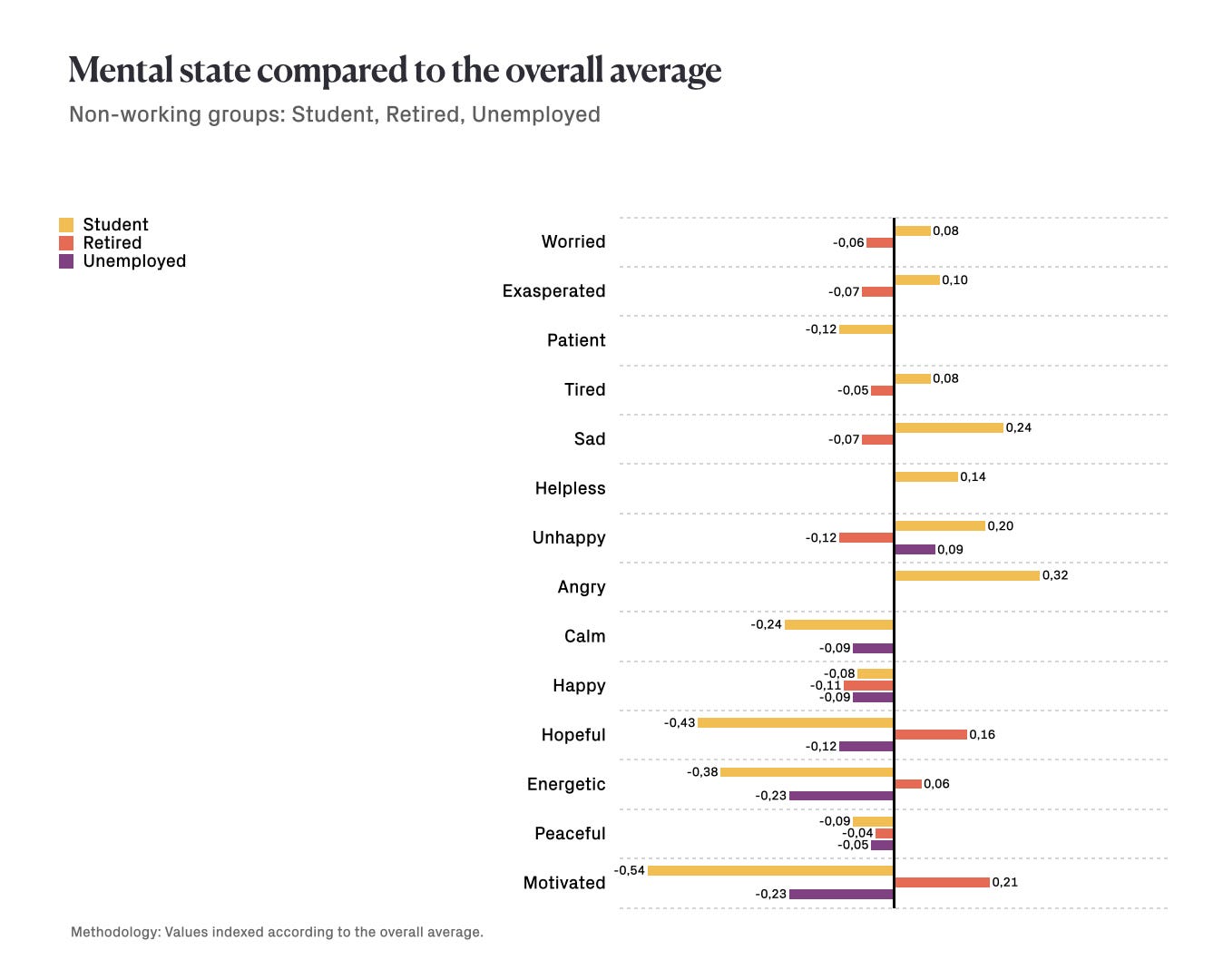

Some insights pertaining to non-working groups, compared to the overall average of all respondents:

- Students are worried, exasperated, and tired. They are also much sadder, unhappier, angrier, and more helpless. Since this is their first time experiencing such a serious and indefinite crisis, students are the group who are emotionally weakest.

- The only group who are relatively better off emotionally are retirees. Here, it's possible to conclude that age and the experience it brings, as well as economic security, are positive factors.

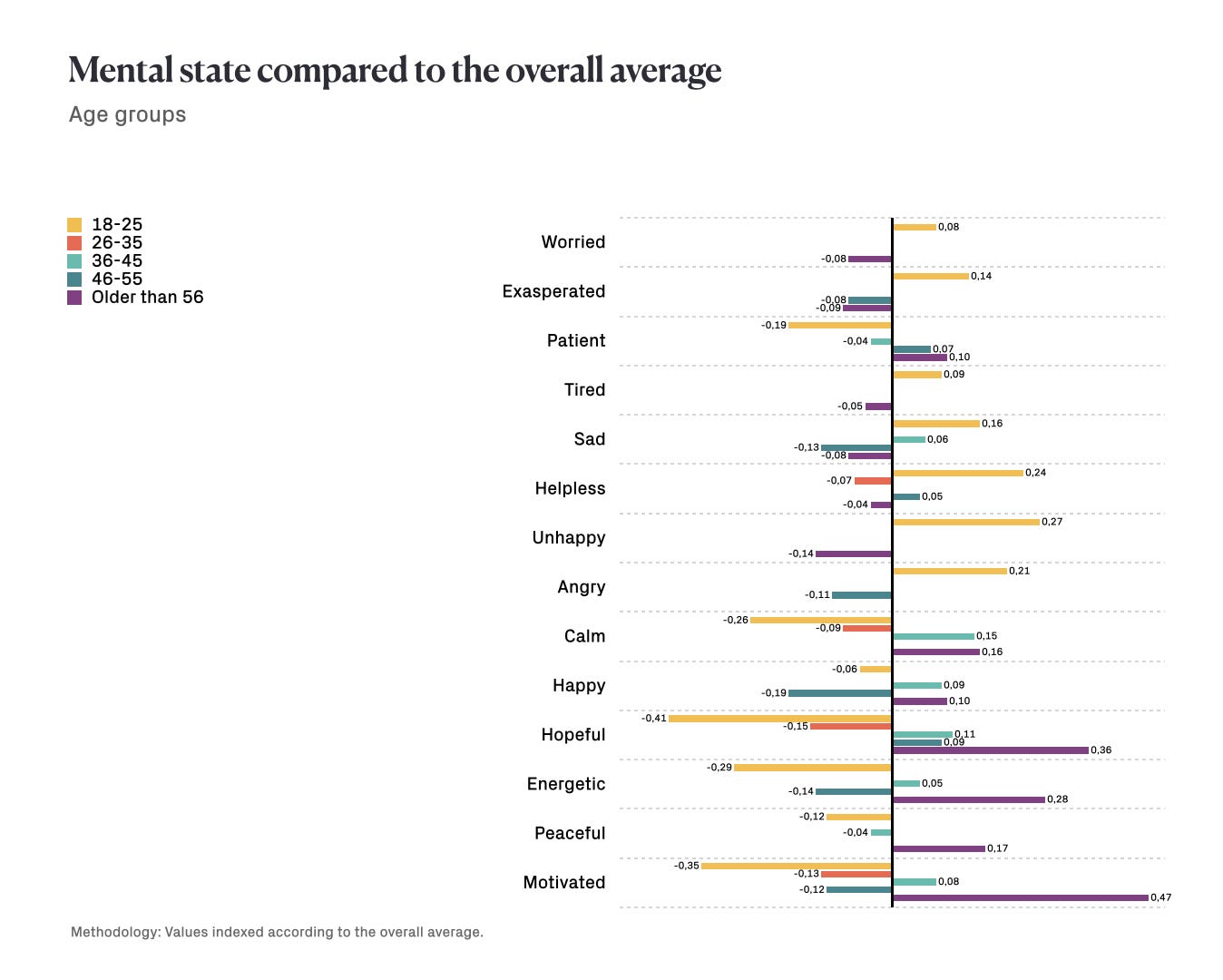

When we look at the age distribution in comparison to the overall average of all respondents, we see that young people are at a greater disadvantage emotionally.

The COVID-19 period is emotionally affecting young people between the ages of 18 and 25 much more seriously than all other age groups.

Meanwhile, those aged 56 and above appear to have a more positive mental state.

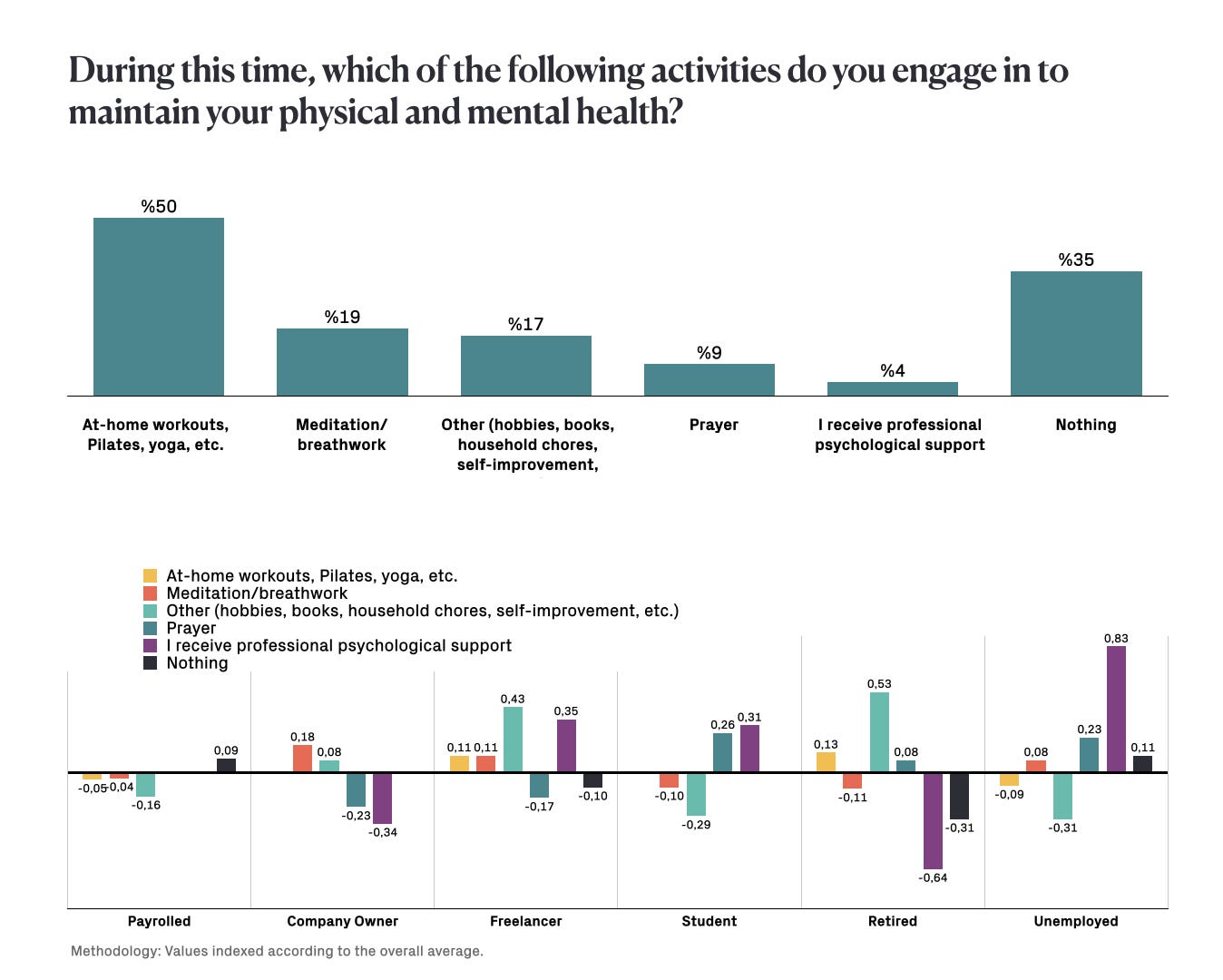

50% of respondents report doing some kind of athletic activity at home during this time.

While 19% are doing meditation/breathwork, 17% are engaged in activities like household chores, hobbies, and reading to maintain their physical and mental health.

9% of respondents report that they engage in prayer, while 4% receive psychological support. 35% of respondents are not engaged in any activities.

When we look at respondents according to their employment status, payrolled employees and company owners rank below the overall average (due to lack of time), while freelancers, students, and retirees can devote more time to activities.

Those who do not engage in any activities to maintain their physical and mental health rank below average in terms of positive feelings and above average in terms of negative feelings.

The greater the number of activities, the more significant improvement can be seen in mental state; while positive feelings become more prominent, negative feelings fade.

No matter what happens, during this time, it seems both effective and necessary for people to make time for themselves and engage in more than one activity to maintain their mental health.

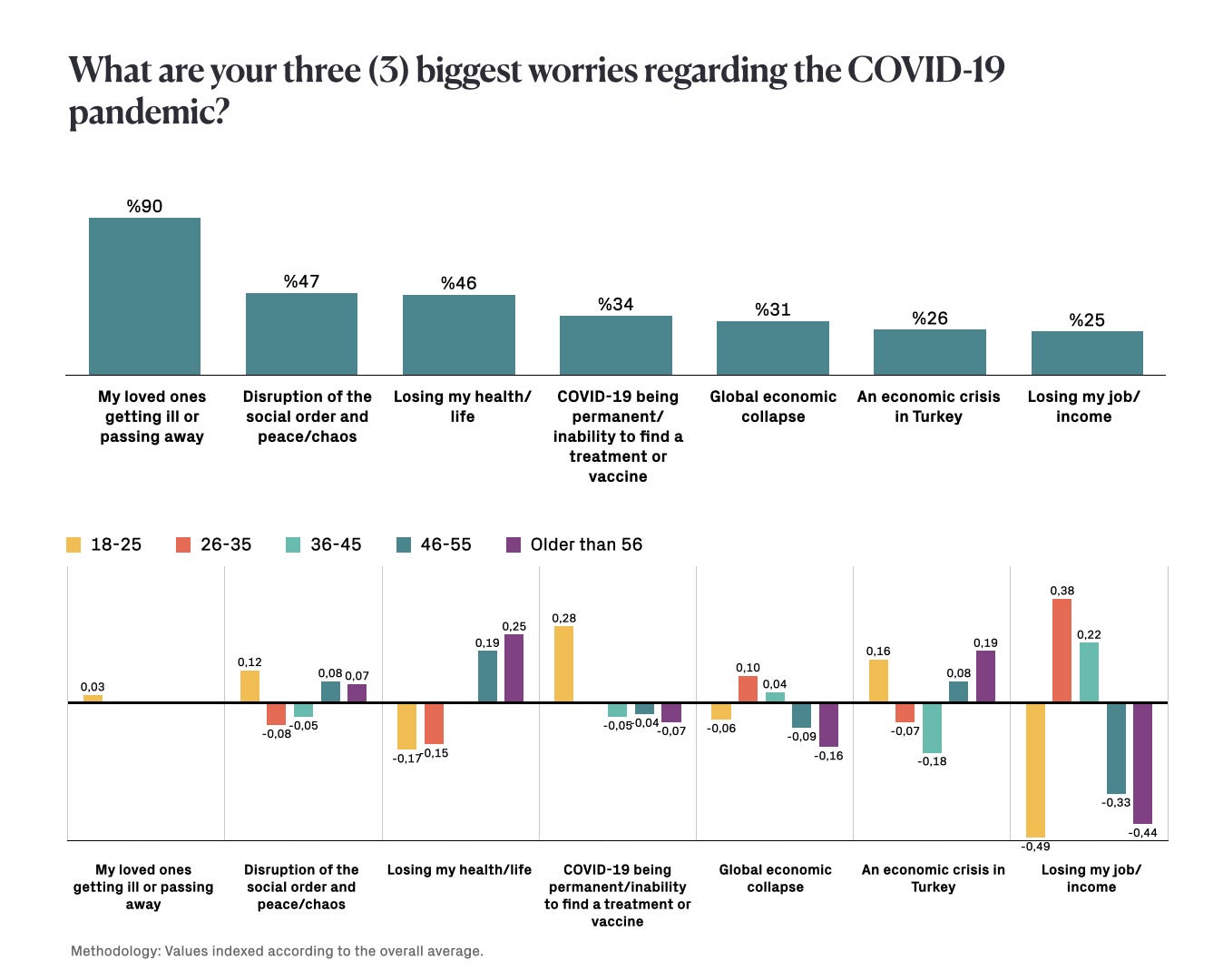

Respondents' greatest worry (as could be expected) is for their loved ones to become ill or pass away.

The other main significant worry - on par with concerns about their own health and livelihood - is the disruption of social order and peace. Respondents fear a state of chaos as much as they fear losing their lives.

Young people and those older than 46 are most afraid of the social order and peace being disrupted.

Concern for a global economic crisis is prominent in the 26–45 age group. Meanwhile, young people and those older than 46 are most worried about an economic crisis in Turkey.

The potential for COVID-19 to be "permanent" frightens young people the most.

The Return to Normal and Expectations

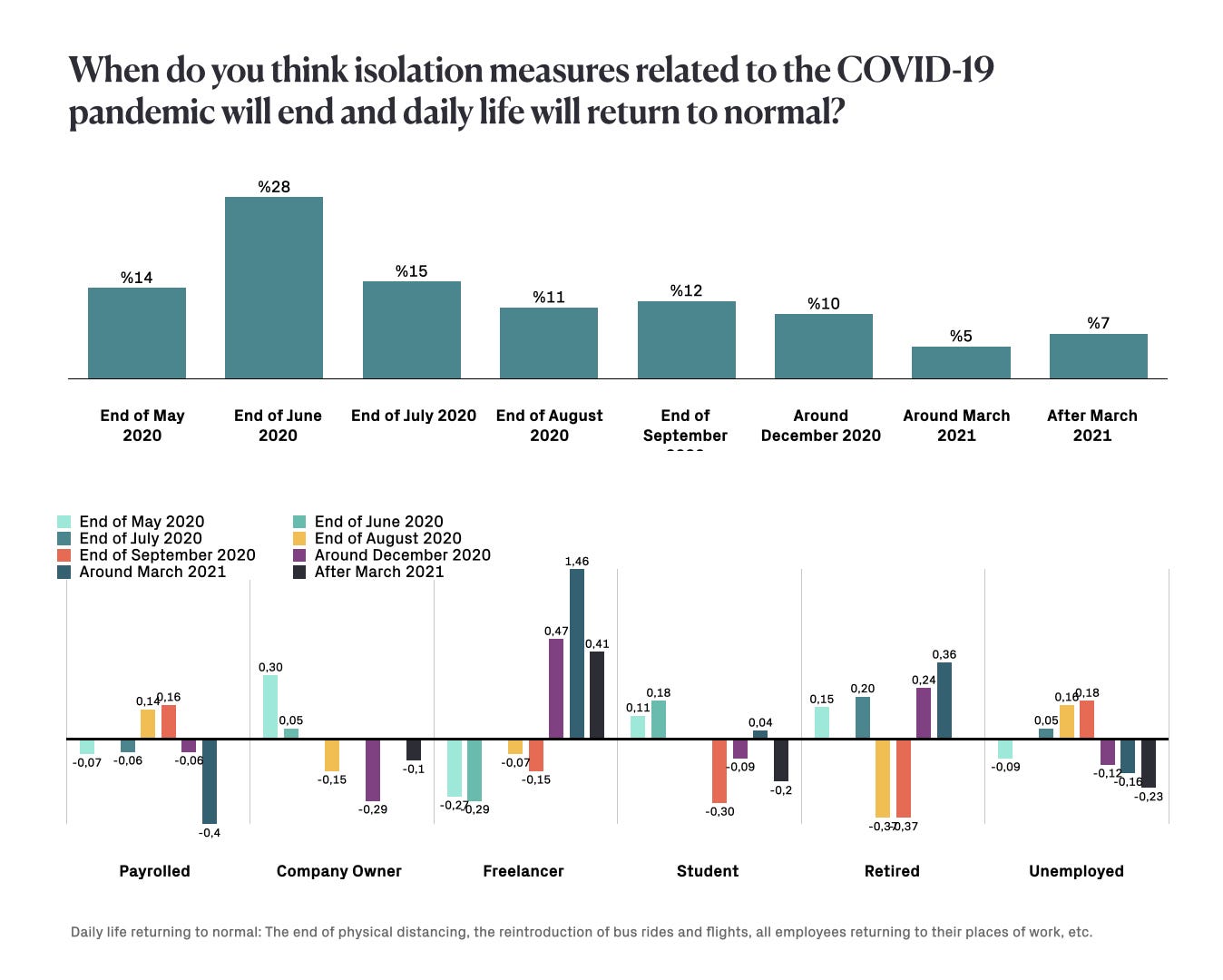

42% of respondents expect to return to "normal" latest by the end of June 2020.

78% expect to return to normal latest by the end of September 2020, while 88% anticipate it will happen latest by the end of 2020. Meanwhile, 12% expect that the return to normal will take place in 2021.

Some insights pertaining to the return to normal, compared to the overall average of all respondents:

- Company owners are the group who expect normalization to occur the earliest, while freelancers share the most pessimistic outlook.

- Payrolled employees consider August-September 2020 a more likely timeframe for normalization.

- While some retirees expect a return to normal during the summer months, others consider the end of 2020 to be more likely.

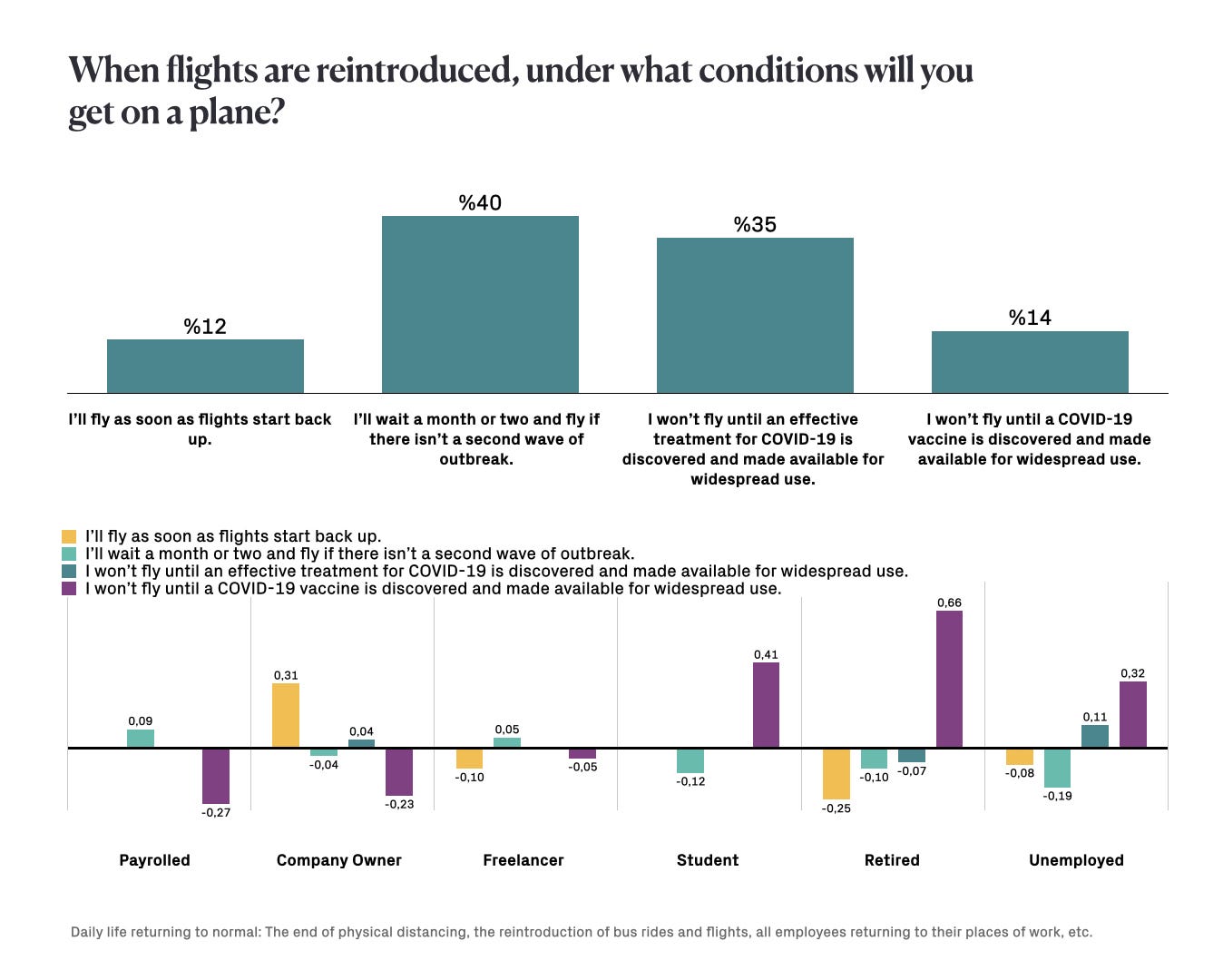

Only 12% of respondents state that they will take a trip as soon as flights start back up.

40% state that they will wait a month or two and take a flight if there isn't a second wave of outbreak, while 58% report that they will not get on a plane until an effective treatment or vaccine is available for widespread use.

Company owners are the only prominent group to state that they will start flying immediately, probably due to the requirements of their job. Meanwhile, students and retirees stand out among those who say they will "not fly without a vaccine."

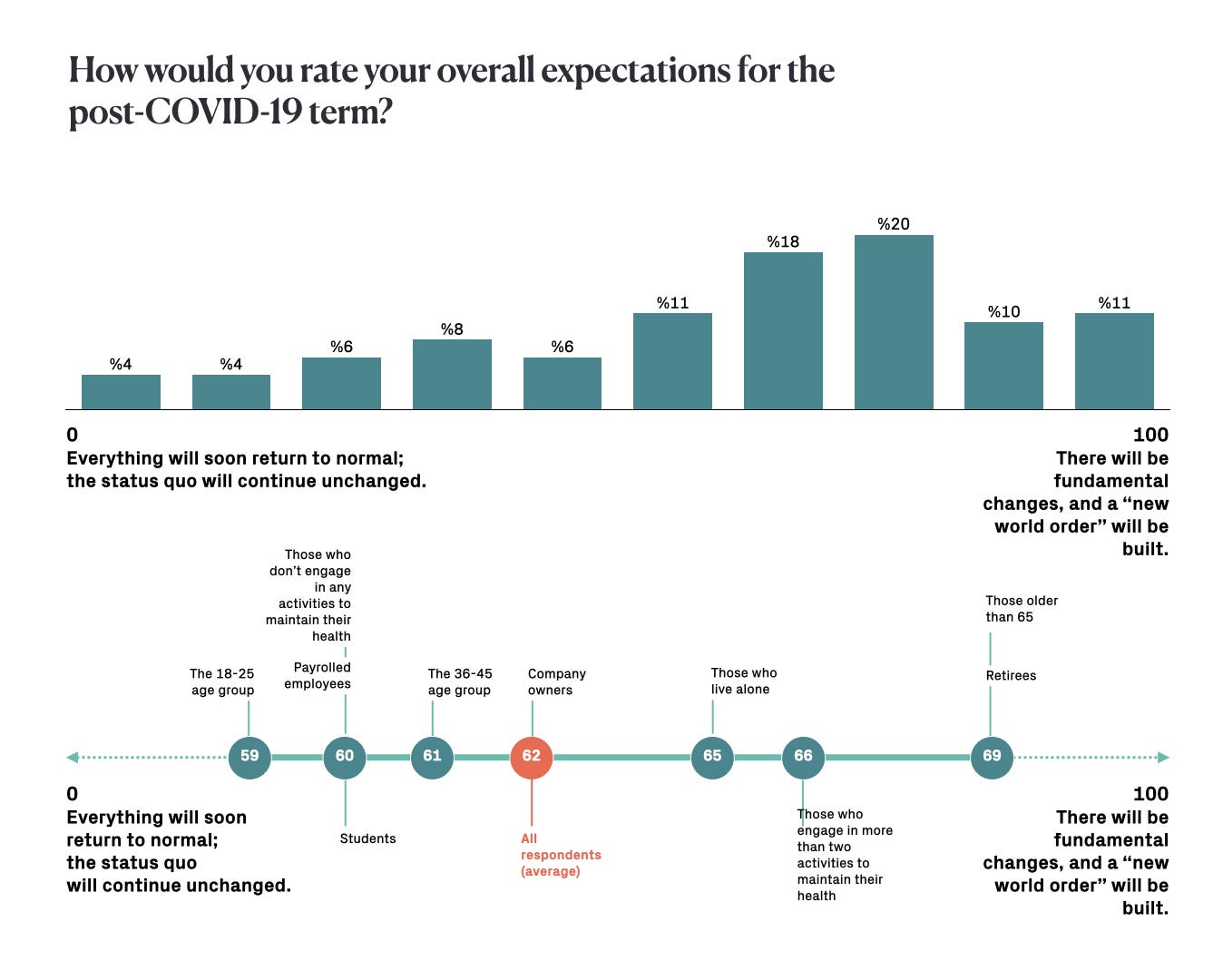

When we take a look at expectations for the post-COVID-19 term, the majority of respondents anticipate some fundamental changes in the system (62 out of 100 on average).

Although there is little expectation that everything will be as it was and the status quo will continue unchanged, those who favor this view (in comparison to the overall average) are those in the 18–25 age group, students, and payrolled employees.

Those expecting more fundamental changes when compared to the overall average are retirees and those older than 65.

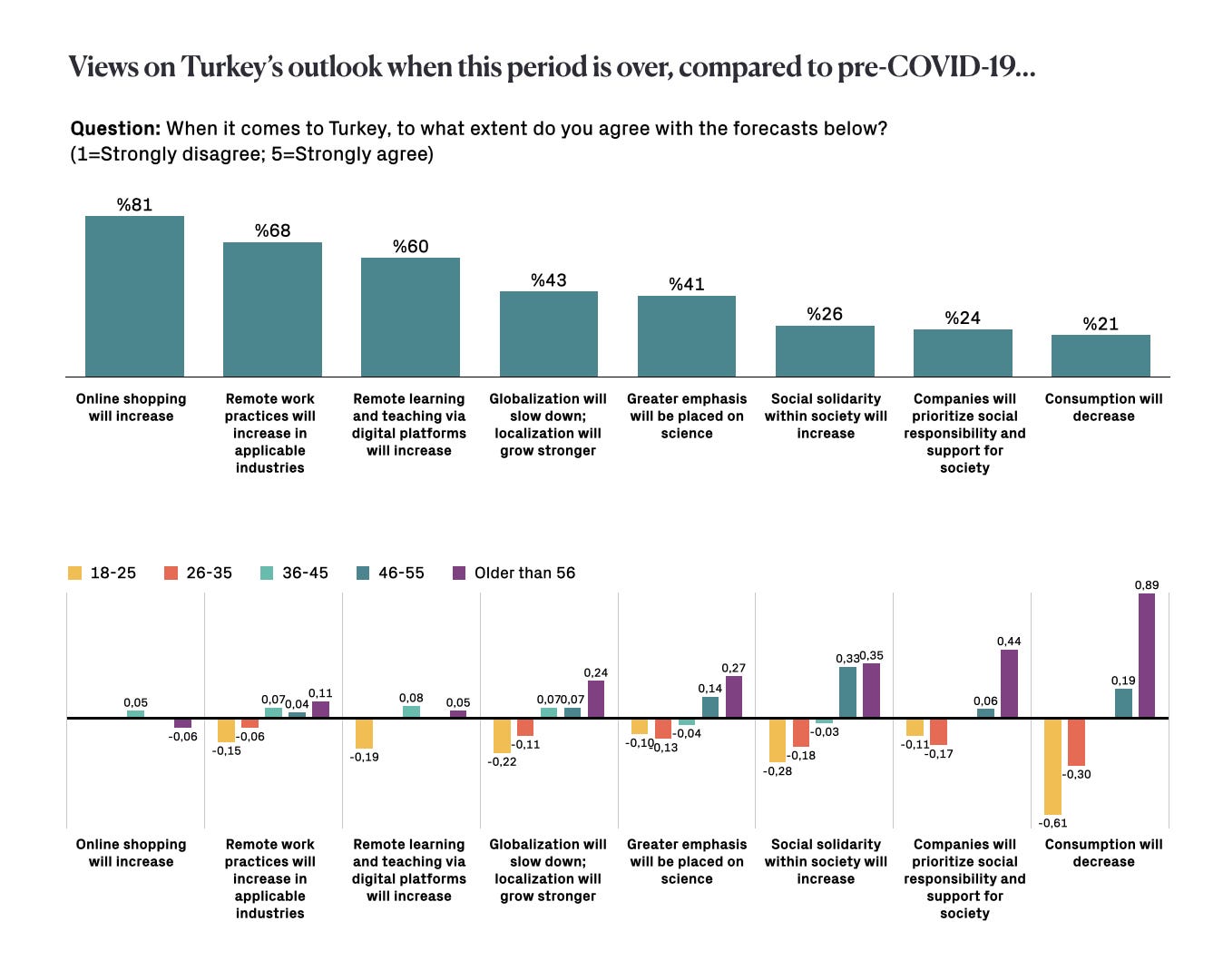

When it comes to expectations for what changes will occur in Turkey, respondents agree overall that there will be an increase in online shopping, remote work, and remote learning.

Meanwhile, there is little expectation that consumption will decrease, that companies will offer greater support for social responsibility, or that social solidarity within society will increase.

When we look at the different age groups, we see that the expectation for change increases in every category (compared to the average) as age increases.

Compared to the average, young people are the group most skeptical of change with the exception of online shopping.

For more detailed information on the survey and to start a dialogue with the ATÖLYE team regarding the needs of your organization during the COVID-19 period, please e-mail collaborate@atolye.io.